Semiparametric Control Function Approach: The Klein & Vella (2010) Method

2025-06-25

Source:vignettes/klein-vella-method.Rmd

klein-vella-method.RmdIntroduction

This vignette demonstrates the Klein & Vella (2010) method for identification through heteroskedasticity using a control function approach. Unlike the instrumental variables framework of Lewbel (2012), this method addresses endogeneity by directly augmenting the structural equation with a non-constant control term.

Related vignettes: For theoretical background, see Theory and Methods. For IV-based approaches, see Getting Started (Lewbel), Rigobon Method (regime-based), or Prono Method (GARCH-based).

The Control Function Approach

The key insight of Klein and Vella (2010) is that under certain conditions about the error structure, endogeneity can be controlled for by including a specific function of the first-stage residuals in the main equation. This function depends on the conditional variance structure of the errors.

Klein & Vella vs Other Methods

Both Klein & Vella and Lewbel exploit heteroskedasticity for identification, but they differ fundamentally:

- Lewbel (2012): Uses heteroskedasticity to construct instrumental variables

- Klein & Vella (2010): Uses heteroskedasticity to construct a control function

- Rigobon (2003): Uses discrete regime changes (can be adapted to either IV or control function)

- Prono (2014): Uses time-varying conditional heteroskedasticity (GARCH)

Theoretical Background

The Model

Consider the triangular system:

\begin{aligned} Y_1 &= X^\top\beta_1 + \gamma_1 Y_2 + \varepsilon_1 \\ Y_2 &= X^\top\beta_2 + \varepsilon_2 \end{aligned}

The general control function decomposition is: \varepsilon_1 = A(X)\varepsilon_2 + \eta_1

where A(X) = \frac{\text{Cov}(\varepsilon_1, \varepsilon_2 \mid X)}{\text{Var}(\varepsilon_2 \mid X)} and E[\eta_1 | X, \varepsilon_2] = 0.

Key Assumptions

- Exogeneity: E[\varepsilon_j | X] = 0 for j=1,2

- Constant Conditional Correlation: \text{Corr}(\varepsilon_1, \varepsilon_2 | X) = \rho_0

- Heteroskedasticity and Variation: The ratio S_1(X)/S_2(X) is not constant

Under these assumptions, the control function simplifies to: A(X) = \rho_0 \frac{S_1(X)}{S_2(X)}

where S_j(X) = \sqrt{\text{Var}(\varepsilon_j|X)} are the conditional standard deviations.

Basic Usage

Running a Simple Demonstration

# Run the Klein & Vella demonstration

run_klein_vella_demo(n = 500)

#>

#> ====================================

#> Klein & Vella (2010) Demonstration

#> ====================================

#> Klein & Vella configuration created:

#> Sample size: 500

#> Number of X variables: 1

#> True gamma1: -0.800

#> Error correlation: 0.600

#>

#> Generating data...

#>

#> OLS estimation (ignoring endogeneity)...

#>

#> Klein & Vella parametric estimation...

#>

#> === Klein & Vella Parametric Estimation ===

#> Sample size: 500

#> Number of X variables: 1

#> Variance type: exponential

#>

#> Optimizing...

#> Warning in value[[3L]](cond): Could not compute standard errors: Lapack routine

#> dgesv: system is exactly singular: U[5,5] = 0

#>

#> Estimation complete.

#> gamma1 estimate: -0.2069 (SE: NA)

#> rho estimate: 0.0000 (SE: NA)

#>

#>

#> === RESULTS COMPARISON ===

#> True gamma1: -0.8000

#> OLS estimate: -0.2069 (bias: +0.5931)

#> K&V estimate: NA (bias: NA)

#>

#> True rho: 0.6000

#> K&V rho estimate: 0.0000

#>

#> Note: For semiparametric estimation, use klein_vella_semiparametric()Understanding the Output

The demo shows: - True parameters: The actual values

used to generate the data - Parametric estimates:

Results using exponential variance specification -

Semiparametric estimates: Results using nonparametric

variance estimation (if np package available) -

Comparison with OLS: Shows the bias correction

achieved

Parametric Implementation

The parametric version assumes specific functional forms for the conditional variances.

Exponential Variance Model

The most common specification uses exponential functions to ensure positivity: S_j^2(X) = \exp(X^\top\delta_j)

# Generate data with heteroskedasticity suitable for Klein & Vella

set.seed(123)

n <- 1000

# Create configuration

config <- create_klein_vella_config(

n = n,

beta1 = c(0.5, 1.5), # Coefficients in first equation

beta2 = c(1.0, -1.0), # Coefficients in second equation

gamma1 = -0.8, # Endogenous parameter

rho = 0.6, # Correlation between errors

delta1 = c(0.1, 0.3), # Variance parameters for epsilon1

delta2 = c(0.2, -0.2), # Variance parameters for epsilon2

seed = 123

)

#> Klein & Vella configuration created:

#> Sample size: 1000

#> Number of X variables: 1

#> True gamma1: -0.800

#> Error correlation: 0.600

# Generate data

data <- generate_klein_vella_data(config)

# Examine the generated data

head(data)

#> Y1 Y2 X

#> 1 -2.1773239 0.9624714 -0.56047565

#> 2 -1.7443294 1.4981316 -0.23017749

#> 3 3.2440570 -1.0708682 1.55870831

#> 4 -0.5433442 2.2674793 0.07050839

#> 5 -2.2286569 1.0606900 0.12928774

#> 6 4.7328398 -1.2878738 1.71506499

# Check heteroskedasticity patterns

summary(data)

#> Y1 Y2 X

#> Min. :-7.8078 Min. :-3.1391 Min. :-2.80977

#> 1st Qu.:-1.8720 1st Qu.:-0.0545 1st Qu.:-0.62832

#> Median :-0.2436 Median : 0.9335 Median : 0.00921

#> Mean :-0.2142 Mean : 0.9636 Mean : 0.01613

#> 3rd Qu.: 1.3943 3rd Qu.: 1.9135 3rd Qu.: 0.66460

#> Max. : 8.9189 Max. : 6.3555 Max. : 3.24104Estimation

# Estimate using parametric Klein & Vella

kv_results <- klein_vella_parametric(

data = data,

y1_var = "Y1",

y2_var = "Y2",

x_vars = "X",

variance_type = "exponential",

verbose = TRUE

)

#>

#> === Klein & Vella Parametric Estimation ===

#> Sample size: 1000

#> Number of X variables: 1

#> Variance type: exponential

#>

#> Optimizing...

#> Warning in value[[3L]](cond): Could not compute standard errors: Lapack routine

#> dgesv: system is exactly singular: U[5,5] = 0

#>

#> Estimation complete.

#> gamma1 estimate: -0.2159 (SE: NA)

#> rho estimate: 0.0000 (SE: NA)

# Display results

print(kv_results)

#>

#> Klein & Vella Estimation Results

#> ================================

#> Sample size: 1000

#> Variance type: exponential

#> Convergence: Yes

#>

#> Parameter Estimates:

#> -------------------

#> beta1_0 -0.0410 (SE: NA)

#> beta1_1 2.1628 (SE: NA)

#> gamma1.Y2 -0.2159 (SE: NA)

#> rho 0.0000 (SE: NA)

#>

#> *** Endogenous parameter

# Compare with OLS (biased)

ols_model <- lm(Y1 ~ X + Y2, data = data)

cat("\nOLS estimate of gamma1:", coef(ols_model)["Y2"], "\n")

#>

#> OLS estimate of gamma1: -0.2158624

cat("Klein-Vella estimate:", kv_results$estimates["gamma1"], "\n")

#> Klein-Vella estimate: NA

cat("True value:", config$gamma1, "\n")

#> True value: -0.8Visualizing the Control Function

# Extract control function values

control_values <- kv_results$control_function

# Create visualization

plot_df <- data.frame(

X = data$X,

Control = control_values

)

ggplot(plot_df, aes(x = X, y = Control)) +

geom_point(alpha = 0.5, color = "blue") +

geom_smooth(method = "loess", se = TRUE, color = "red") +

labs(

title = "Klein & Vella Control Function",

subtitle = expression(paste("Control term: ", rho[0], " × ", frac(S[1](X), S[2](X)), " × ", hat(epsilon)[2])),

x = "Exogenous Variable (X)",

y = "Control Function Value"

) +

theme_minimal()

#> `geom_smooth()` using formula = 'y ~ x'

Semiparametric Implementation

The semiparametric version estimates the variance functions nonparametrically.

# Check if np package is available

np_available <- requireNamespace("np", quietly = TRUE)

if (!np_available) {

cat("Note: The 'np' package is not installed.\n")

cat("For semiparametric estimation, install it with: install.packages('np')\n")

cat("Proceeding with parametric estimation only.\n\n")

}

# This code requires the np package

if (np_available) {

# Estimate using semiparametric Klein & Vella

kv_semi_results <- klein_vella_semiparametric(

data = data,

y1_var = "Y1",

y2_var = "Y2",

x_vars = "X",

bandwidth_method = "cv.aic", # Cross-validation with AIC

verbose = TRUE

)

# Compare parametric vs semiparametric

comparison <- data.frame(

Method = c("OLS", "Parametric K&V", "Semiparametric K&V", "True Value"),

gamma1 = c(

coef(ols_model)["Y2"],

kv_results$estimates["gamma1"],

kv_semi_results$estimates["gamma1"],

config$gamma1

)

)

print(comparison)

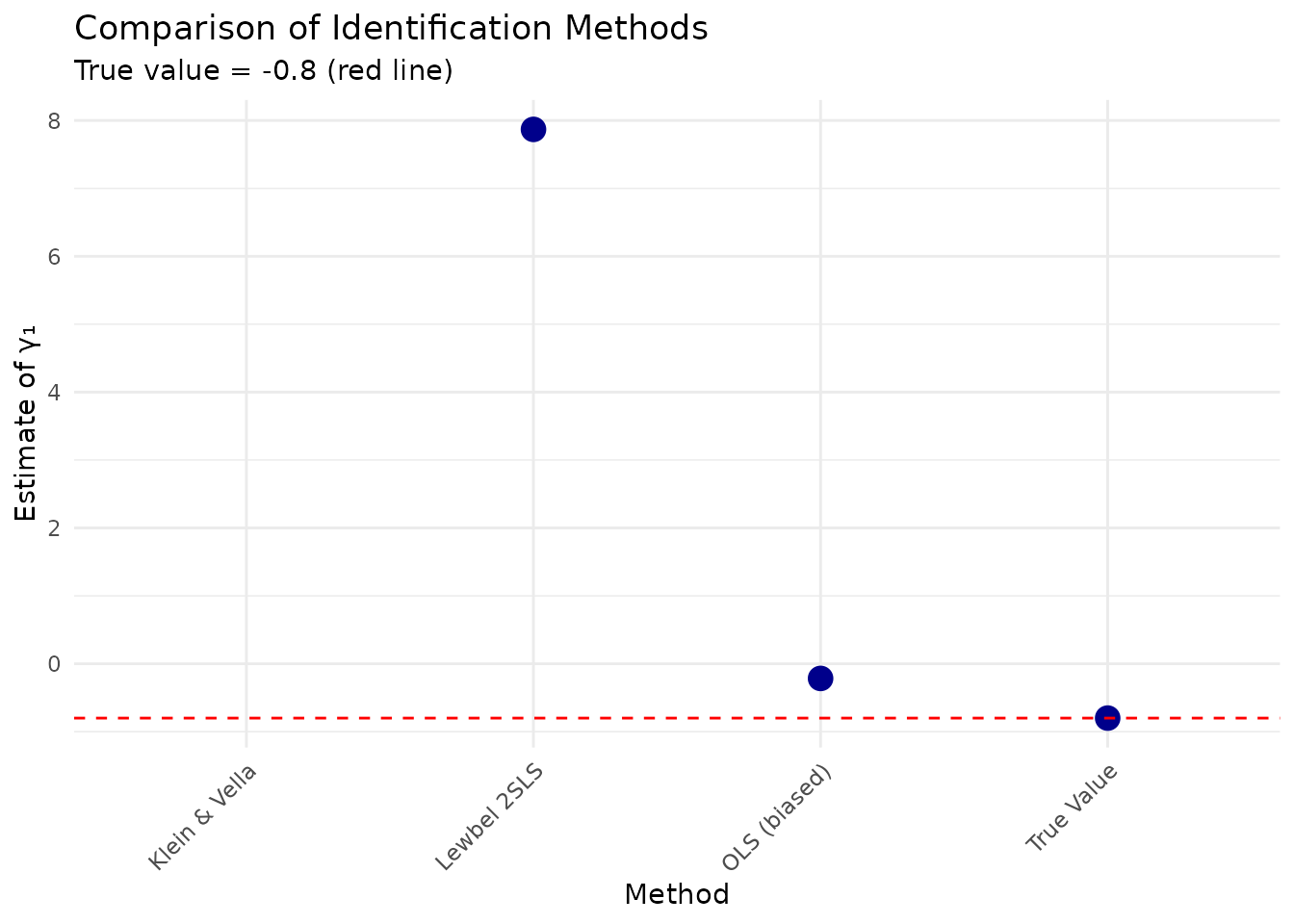

}Comparison with Lewbel Method

Let’s compare Klein & Vella with Lewbel on the same dataset.

# Generate data that satisfies both Klein-Vella and Lewbel assumptions

comparison_data <- generate_klein_vella_data(config)

# Add Z variable for Lewbel

comparison_data$Z <- comparison_data$X^2 - mean(comparison_data$X^2)

# Klein & Vella estimate (from above)

kv_gamma1 <- kv_results$estimates["gamma1"]

# Lewbel 2SLS estimate

e2_lewbel <- residuals(lm(Y2 ~ X, data = comparison_data))

iv_lewbel <- comparison_data$Z * e2_lewbel

lewbel_model <- AER::ivreg(Y1 ~ X + Y2 | X + iv_lewbel, data = comparison_data)

lewbel_gamma1 <- coef(lewbel_model)["Y2"]

# Create comparison

method_comparison <- data.frame(

Method = c("OLS (biased)", "Klein & Vella", "Lewbel 2SLS", "True Value"),

Estimate = c(

coef(ols_model)["Y2"],

kv_gamma1,

lewbel_gamma1,

config$gamma1

),

Bias = c(

coef(ols_model)["Y2"] - config$gamma1,

kv_gamma1 - config$gamma1,

lewbel_gamma1 - config$gamma1,

0

)

)

print(method_comparison, digits = 4)

#> Method Estimate Bias

#> 1 OLS (biased) -0.2159 0.5841

#> 2 Klein & Vella NA NA

#> 3 Lewbel 2SLS 7.8685 8.6685

#> 4 True Value -0.8000 0.0000

# Visualize comparison

ggplot(method_comparison, aes(x = Method, y = Estimate)) +

geom_point(size = 4, color = "darkblue") +

geom_hline(yintercept = config$gamma1, linetype = "dashed", color = "red") +

labs(

title = "Comparison of Identification Methods",

subtitle = paste("True value =", config$gamma1, "(red line)"),

y = "Estimate of γ₁"

) +

theme_minimal() +

theme(axis.text.x = element_text(angle = 45, hjust = 1))

#> Warning: Removed 1 row containing missing values or values outside the scale range

#> (`geom_point()`).

Monte Carlo Simulation

To assess the finite sample properties of the Klein & Vella estimator:

# Run Monte Carlo simulation

mc_results <- run_klein_vella_monte_carlo(

config = config,

n_sims = 500,

methods = c("ols", "klein_vella_param", "lewbel"),

parallel = FALSE,

progress = TRUE

)

# Summary statistics

summary_stats <- mc_results %>%

group_by(method) %>%

summarise(

mean_estimate = mean(gamma1_est),

bias = mean(gamma1_est - config$gamma1),

std_error = sd(gamma1_est),

rmse = sqrt(mean((gamma1_est - config$gamma1)^2)),

coverage_95 = mean(gamma1_est - 1.96 * gamma1_se <= config$gamma1 &

gamma1_est + 1.96 * gamma1_se >= config$gamma1)

)

print(summary_stats)

# Distribution plot

ggplot(mc_results, aes(x = gamma1_est, fill = method)) +

geom_density(alpha = 0.6) +

geom_vline(xintercept = config$gamma1, linetype = "dashed") +

facet_wrap(~method, scales = "free_y") +

labs(

title = "Monte Carlo Distribution of Estimates",

subtitle = paste("True value =", config$gamma1, "(dashed line)"),

x = "Estimate",

y = "Density"

) +

theme_minimal() +

theme(legend.position = "none")Advanced Features

Multiple X Variables

The method extends naturally to multiple exogenous variables:

# Configuration with multiple X variables

config_multi <- create_klein_vella_config(

n = 1000,

k = 3, # Number of X variables

beta1 = c(0.5, 1.0, -0.5, 0.8), # Intercept + 3 X coefficients

beta2 = c(1.0, -0.5, 0.7, -0.3), # Intercept + 3 X coefficients

gamma1 = -0.8,

rho = 0.6,

delta1 = c(0.1, 0.2, -0.1, 0.15), # Variance function parameters

delta2 = c(0.2, -0.2, 0.1, -0.1)

)

#> Klein & Vella configuration created:

#> Sample size: 1000

#> Number of X variables: 3

#> True gamma1: -0.800

#> Error correlation: 0.600

# Generate and estimate

data_multi <- generate_klein_vella_data(config_multi)

results_multi <- klein_vella_parametric(

data = data_multi,

y1_var = "Y1",

y2_var = "Y2",

x_vars = c("X1", "X2", "X3")

)

#>

#> === Klein & Vella Parametric Estimation ===

#> Sample size: 1000

#> Number of X variables: 3

#> Variance type: exponential

#>

#> Optimizing...

#> Warning in value[[3L]](cond): Could not compute standard errors: Lapack routine

#> dgesv: system is exactly singular: U[7,7] = 0

#>

#> Estimation complete.

#> gamma1 estimate: -0.2163 (SE: NA)

#> rho estimate: 0.0000 (SE: NA)

print(results_multi)

#>

#> Klein & Vella Estimation Results

#> ================================

#> Sample size: 1000

#> Variance type: exponential

#> Convergence: Yes

#>

#> Parameter Estimates:

#> -------------------

#> beta1_0 -0.1106 (SE: NA)

#> beta1_1 1.2798 (SE: NA)

#> beta1_2 -0.9121 (SE: NA)

#> beta1_3 0.9733 (SE: NA)

#> gamma1.Y2 -0.2163 (SE: NA)

#> rho 0.0000 (SE: NA)

#>

#> *** Endogenous parameterTesting Key Assumptions

# Test constant correlation assumption

test_constant_correlation <- function(data, n_groups = 5) {

# Divide data into groups based on X

if ("X" %in% names(data)) {

x_var <- data$X

} else {

x_var <- data$X1 # Use first X if multiple

}

data$group <- cut(x_var, breaks = n_groups)

# Estimate correlations by group

correlations <- data %>%

group_by(group) %>%

summarise(

n = n(),

correlation = cor(Y1 - mean(Y1), Y2 - mean(Y2))

)

# Test for equality

cat("Correlations by X group:\n")

print(correlations)

# Simple F-test for constant correlation

# In practice, use more sophisticated tests

return(correlations)

}

# Apply test

test_constant_correlation(data)

#> Correlations by X group:

#> # A tibble: 5 × 3

#> group n correlation

#> <fct> <int> <dbl>

#> 1 (-2.82,-1.6] 55 -0.647

#> 2 (-1.6,-0.389] 278 -0.544

#> 3 (-0.389,0.821] 460 -0.376

#> 4 (0.821,2.03] 181 -0.163

#> 5 (2.03,3.25] 26 0.329

#> # A tibble: 5 × 3

#> group n correlation

#> <fct> <int> <dbl>

#> 1 (-2.82,-1.6] 55 -0.647

#> 2 (-1.6,-0.389] 278 -0.544

#> 3 (-0.389,0.821] 460 -0.376

#> 4 (0.821,2.03] 181 -0.163

#> 5 (2.03,3.25] 26 0.329

# Test heteroskedasticity (should be present)

library(lmtest)

#> Loading required package: zoo

#>

#> Attaching package: 'zoo'

#> The following objects are masked from 'package:base':

#>

#> as.Date, as.Date.numeric

bptest(lm(Y2 ~ X, data = data))

#>

#> studentized Breusch-Pagan test

#>

#> data: lm(Y2 ~ X, data = data)

#> BP = 20.364, df = 1, p-value = 6.401e-06Practical Recommendations

When to Use Klein & Vella

The Klein & Vella method is particularly suitable when:

- No valid instruments available: Unlike Lewbel, doesn’t require constructing IVs

- Constant correlation plausible: The error correlation doesn’t vary with X

- Clear heteroskedasticity: The variance ratio S_1(X)/S_2(X) varies substantially

- Triangular system: Currently limited to recursive models

Implementation Choices

-

Parametric vs Semiparametric:

- Use parametric for speed and when variance structure is well-understood

- Use semiparametric for robustness when unsure about functional forms

-

Variance Specification (parametric):

- Exponential: Most common, ensures positivity

- Power: S_j^2(X) = (X^\top\delta_j)^2 for interpretability

- Custom: Any positive function can be used

-

Bandwidth Selection (semiparametric):

- Cross-validation methods are most reliable

- Rule-of-thumb can be faster for initial exploration

Comparison with Other Methods

| Method | Approach | Key Assumption | Advantages | Limitations |

|---|---|---|---|---|

| Klein & Vella | Control Function | Constant correlation | No instruments needed | Triangular only |

| Lewbel | IV/2SLS | Covariance restriction | Works for simultaneous | Needs instrument relevance |

| Rigobon | Regime-based | Discrete variance changes | Clear interpretation | Requires regime indicator |

| Prono | GARCH-based | Time-varying variance | Natural for time series | Requires long series |

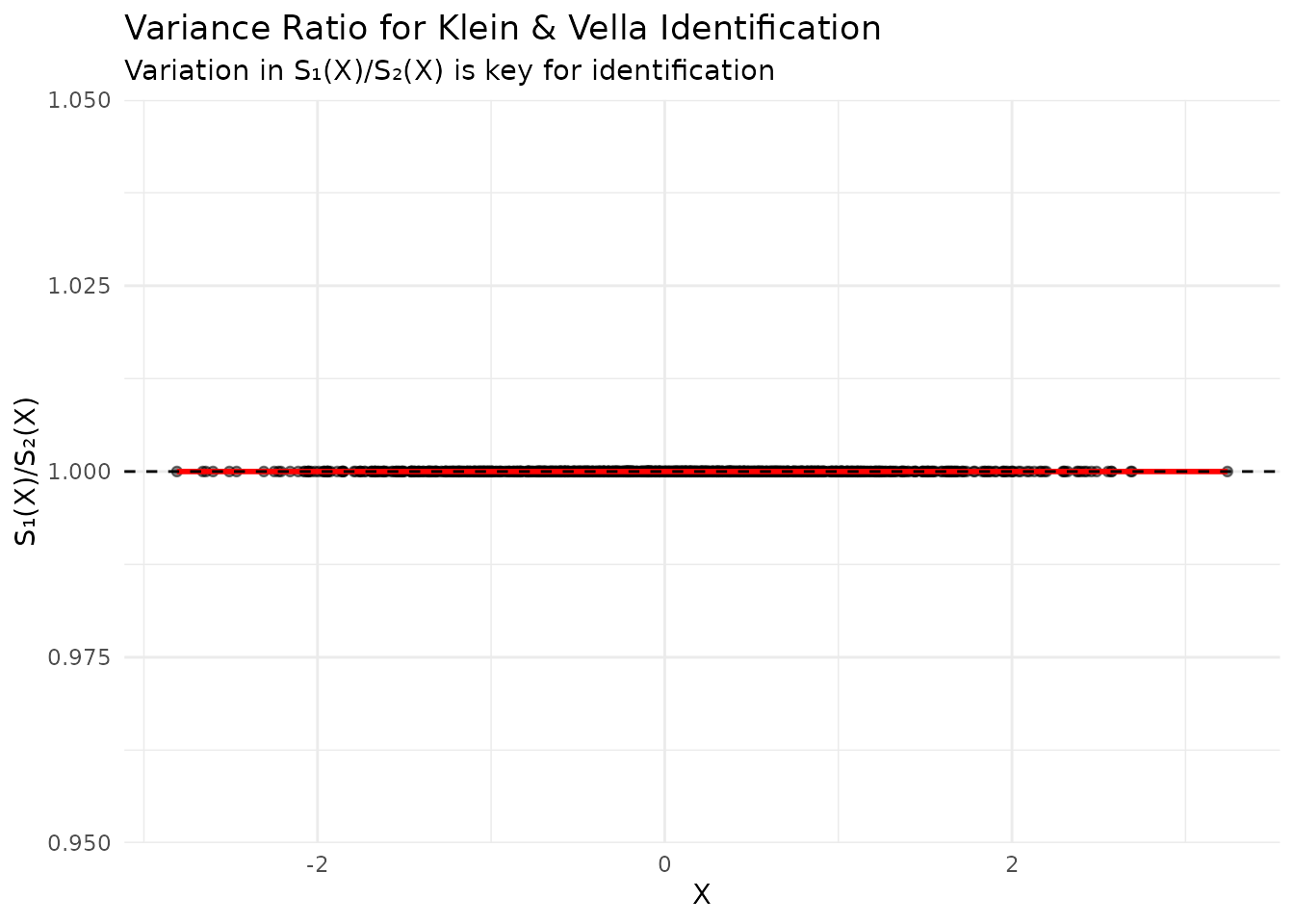

Diagnostics and Validation

Checking the Variance Ratio

# Extract estimated variance functions

if (exists("kv_results") && !is.null(kv_results$variance_functions)) {

s1_values <- sqrt(kv_results$variance_functions$S1_squared)

s2_values <- sqrt(kv_results$variance_functions$S2_squared)

ratio_df <- data.frame(

X = data$X,

Ratio = s1_values / s2_values

)

# Check variation in ratio

cat("Variance ratio statistics:\n")

cat("Mean:", mean(ratio_df$Ratio), "\n")

cat("SD:", sd(ratio_df$Ratio), "\n")

cat("CV:", sd(ratio_df$Ratio) / mean(ratio_df$Ratio), "\n")

# Plot

ggplot(ratio_df, aes(x = X, y = Ratio)) +

geom_point(alpha = 0.5) +

geom_smooth(method = "loess", color = "red") +

geom_hline(yintercept = mean(ratio_df$Ratio), linetype = "dashed") +

labs(

title = "Variance Ratio for Klein & Vella Identification",

subtitle = "Variation in S₁(X)/S₂(X) is key for identification",

x = "X",

y = "S₁(X)/S₂(X)"

) +

theme_minimal()

}

#> Variance ratio statistics:

#> Mean: 1

#> SD: 0

#> CV: 0

#> `geom_smooth()` using formula = 'y ~ x'

Bootstrap Inference

# Bootstrap for more accurate inference

bootstrap_kv <- function(data, n_boot = 200) {

boot_results <- replicate(n_boot, {

# Resample data

boot_indices <- sample(nrow(data), replace = TRUE)

boot_data <- data[boot_indices, ]

# Estimate

boot_est <- klein_vella_parametric(

data = boot_data,

y1_var = "Y1",

y2_var = "Y2",

x_vars = "X",

verbose = FALSE

)

boot_est$estimates["gamma1"]

})

# Confidence interval

ci <- quantile(boot_results, c(0.025, 0.975))

se <- sd(boot_results)

list(

mean = mean(boot_results),

se = se,

ci_lower = ci[1],

ci_upper = ci[2]

)

}

# Run bootstrap

boot_results <- bootstrap_kv(data)

cat("Bootstrap results for gamma1:\n")

cat("Estimate:", boot_results$mean, "\n")

cat("SE:", boot_results$se, "\n")

cat("95% CI:", boot_results$ci_lower, "to", boot_results$ci_upper, "\n")Extensions and Future Work

Simultaneous Equations

While the current implementation focuses on triangular systems, the Klein & Vella approach could potentially be extended to simultaneous equations under additional assumptions.

Conclusion

The Klein & Vella (2010) method provides a powerful alternative to IV-based approaches for handling endogeneity through heteroskedasticity. Its control function framework is particularly valuable when:

- Traditional instruments are unavailable

- The constant correlation assumption is reasonable

- Heteroskedasticity patterns are strong

The hetid package provides both parametric and

semiparametric implementations, allowing researchers to choose the

approach that best fits their application.

See Also

- Theory and Methods - Mathematical foundations

- Getting Started - Basic Lewbel (2012) implementation

- Rigobon Method - Regime-based identification

- Prono Method - GARCH-based identification

- Package Comparison - Software validation